Example usage

Here we will demonstrat how to use pyredraw to construct replicate times series by performing the moving block bootstrap.

An application of the moving block bootstrap function from pyredraw will be shown. The application will be to a seasonal time series and will follow the general approach by Bergmeir et al.$^1$

Starting with a given seasonal time series in the upper left of the diagram, we will perform a Box-Cox transform, followed by a STL decomposition. With the residuals resulting from the STL decomposition, replicate residuals will be formed and which are highlighted in a yellow box in the diagram. These replicate residuals are created by using the moving_block_bootstrap() function from pyredraw.

With each of the bootsrapped residual replicates, we will then add back the trend and seasonality time series components found from the STL decomposition, and perform an inverse Box-Cox transform to obtain a bootstrapped replicate of the original time series.

Import packages, time series data, and create a Numpy array

import pandas as pd

import numpy as np

from scipy.stats import boxcox

from scipy.special import inv_boxcox

from statsmodels.tsa.seasonal import STL

import matplotlib.pyplot as plt

from pyredraw.ts import moving_block_bootstrap

from pyredraw.plotting import plot_replicates

# read in time series data

df = pd.read_csv("iceland_montly_retail_debit_card_expenditures.csv",

index_col='date',

parse_dates=True

)

df.head()

| monthly_expenditure | |

|---|---|

| date | |

| 2000-01-01 | 7.204 |

| 2000-02-01 | 7.335 |

| 2000-03-01 | 7.812 |

| 2000-04-01 | 7.413 |

| 2000-05-01 | 9.136 |

# create pandas series, add frequency of time index (Monthly, Starting)

sr = df.squeeze()

sr = sr.asfreq('MS')

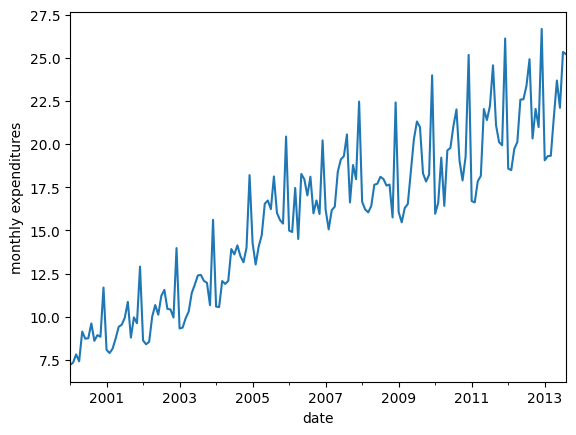

# plot time series - time series shows clear seasonality

ax = sr.plot()

ax.set_ylabel("monthly expenditures")

plt.show()

sr.values

array([ 7.204, 7.335, 7.812, 7.413, 9.136, 8.725, 8.751, 9.609,

8.601, 8.93 , 8.835, 11.688, 8.078, 7.892, 8.151, 8.738,

9.416, 9.533, 9.943, 10.859, 8.789, 9.96 , 9.619, 12.9 ,

8.62 , 8.401, 8.546, 10.004, 10.675, 10.115, 11.206, 11.555,

10.453, 10.421, 9.95 , 13.975, 9.315, 9.366, 9.91 , 10.302,

11.371, 11.857, 12.387, 12.421, 12.073, 11.963, 10.666, 15.613,

10.586, 10.558, 12.064, 11.899, 12.077, 13.918, 13.611, 14.132,

13.509, 13.152, 13.993, 18.203, 14.262, 13.024, 14.062, 14.718,

16.544, 16.732, 16.23 , 18.126, 16.016, 15.601, 15.394, 20.439,

14.991, 14.908, 17.459, 14.501, 18.271, 17.963, 17.026, 18.111,

15.989, 16.735, 15.949, 20.216, 16.198, 15.06 , 16.168, 16.376,

18.403, 19.113, 19.303, 20.56 , 16.621, 18.788, 17.97 , 22.464,

16.658, 16.214, 16.043, 16.418, 17.644, 17.705, 18.107, 17.975,

17.598, 17.658, 15.75 , 22.414, 16.065, 15.467, 16.297, 16.53 ,

18.41 , 20.274, 21.311, 20.991, 18.305, 17.832, 18.223, 23.987,

15.964, 16.606, 19.216, 16.419, 19.638, 19.773, 21.052, 22.011,

19.039, 17.893, 19.276, 25.167, 16.699, 16.619, 17.851, 18.16 ,

22.032, 21.395, 22.217, 24.565, 21.095, 20.114, 19.931, 26.12 ,

18.58 , 18.492, 19.724, 20.123, 22.582, 22.595, 23.379, 24.92 ,

20.325, 22.038, 20.988, 26.675, 19.061, 19.303, 19.323, 21.573,

23.685, 22.104, 25.34 , 25.211])

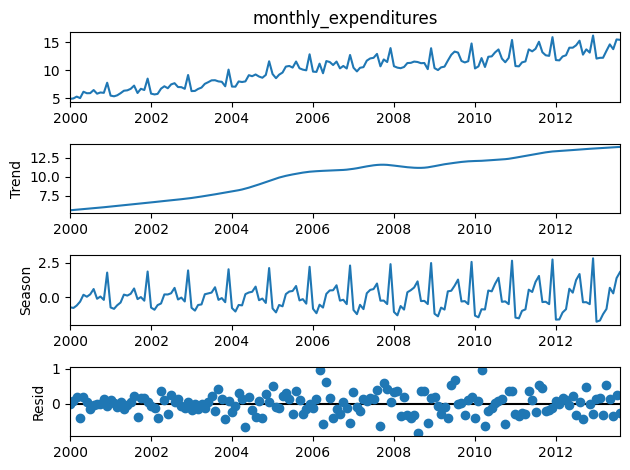

Perform Box-Cox transform and STL decomposition on transformed result

# Do box-cox transform

boxcox_array, lambda_val = boxcox(sr.values)

# make series from array resulting from box-cox

boxcox_series = pd.Series(

boxcox_array, index=pd.date_range("1-1-2000", periods=len(boxcox_array), freq="MS")

, name="monthly_expenditures"

)

# do STL decomp (note seasonal = period+1, seasonal must be odd)

period=12

stl = STL(boxcox_series, seasonal=(period+1))

stl_result = stl.fit()

# Plot STL decomposition results

fig = stl_result.plot()

Apply moving_block_bootstrap from the pyredraw package to STL residuals

# define parameters for moving block bootstrap

block_length = int(2 * period)

number_replicates = 10

# do moving block bootstrap of STL residuals

residual_replicates = moving_block_bootstrap(stl_result.resid,

block_length,

number_replicates,

seed = 1027)

residual_replicates.shape

(10, 164)

# make residual array into pandas dataframe

# adding back seasonal and trend from STL, do inverse Box-Cox

df_replicates = pd.DataFrame(columns=["monthly_expenditures", "replicate"])

number_replicates, _ = residual_replicates.shape

number_replicates_array = np.arange(0, number_replicates)

for replicate in number_replicates_array:

# make residual in a pandas series with correct datetime index

sr_temp = pd.Series(residual_replicates[replicate,],

index=pd.date_range("1-1-2000",

periods=len(residual_replicates[replicate,]),

freq="MS"),

name="monthly_expenditures"

)

# add seasonal and trend components from STL to residual replicate

sr_total_temp = sr_temp + stl_result.seasonal + stl_result.trend

sr_total_temp =sr_total_temp.rename("monthly_expenditures")

# do inverse Box-Cox (using exponent lambda that was found in the initial Box Cox)

sr_inv_boxcox = inv_boxcox(sr_total_temp, lambda_val)

# make pandas series into temp dataframe and add replicate field

df_temp = pd.DataFrame(sr_inv_boxcox)

df_temp["replicate"] = replicate

# concatenate

df_replicates = pd.concat([df_replicates, df_temp])

df_replicates.info()

df_replicates.head()

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 1640 entries, 2000-01-01 to 2013-08-01

Data columns (total 2 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 monthly_expenditures 1640 non-null float64

1 replicate 1640 non-null object

dtypes: float64(1), object(1)

memory usage: 38.4+ KB

| monthly_expenditures | replicate | |

|---|---|---|

| 2000-01-01 | 6.639942 | 0 |

| 2000-02-01 | 6.726259 | 0 |

| 2000-03-01 | 6.302820 | 0 |

| 2000-04-01 | 8.579374 | 0 |

| 2000-05-01 | 9.398532 | 0 |

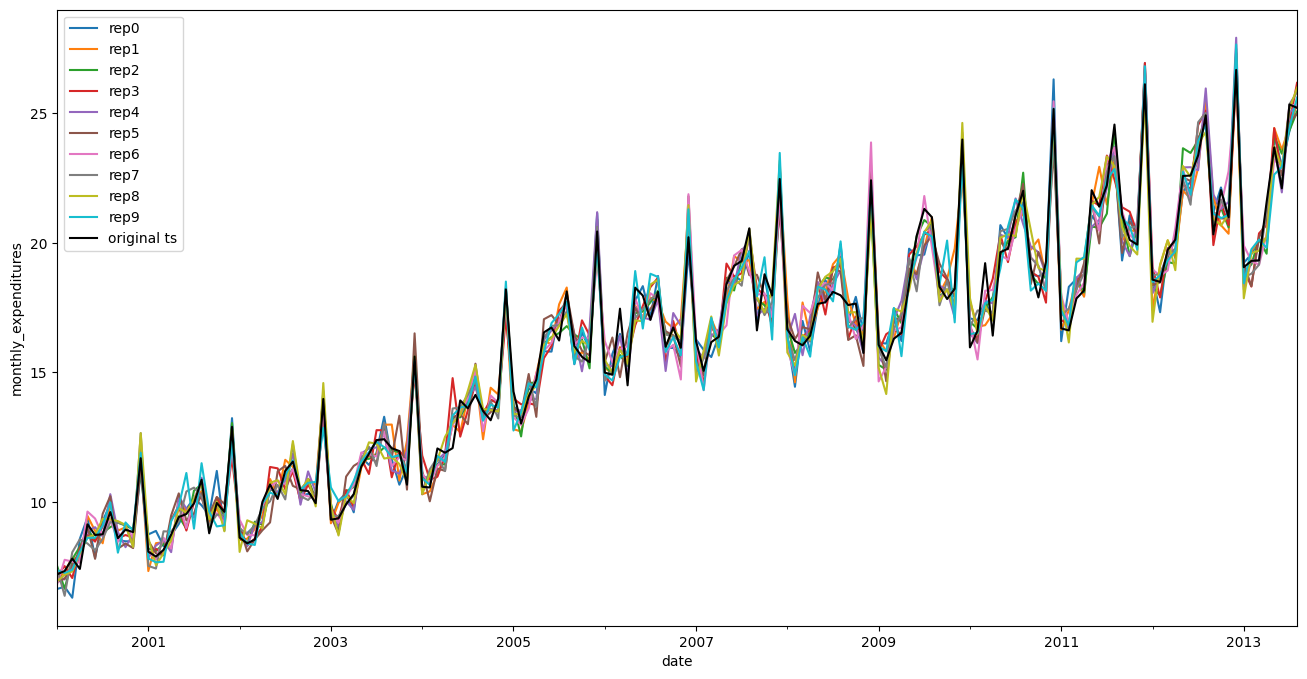

Plot replicates and original time series on same axis to compare

# Plot replicates and original time series

plot_replicates(sr, df_replicates, "monthly_expenditures")

Citation:

C. Bergmeir, R. J. Hyndman, and J. M. Ben´ıtez, “Bagging exponential smoothing methods using STL decomposition and Box–Cox transformation,” International journal of forecasting, vol. 32, no. 2, pp. 303–312, 2016.